How do you solve a problem like inflation?

A holistic stabilisation toolkit fit for the 21st century

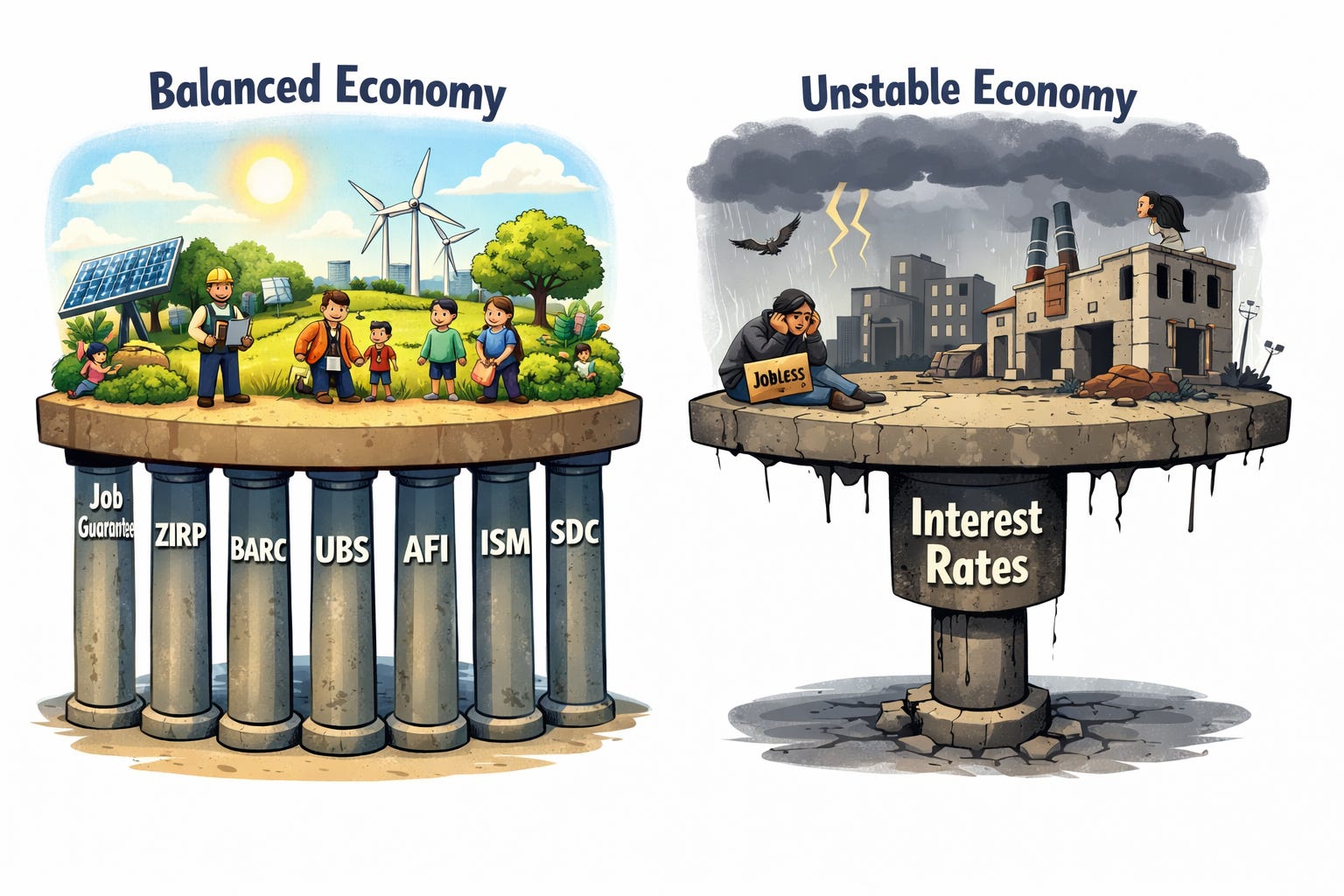

The UK’s existing macroeconomic stabilisation regime can be summarised, bluntly, as ‘if inflation rises, someone must lose their job’. The policy lever to enact this is the central bank policy interest rate, and the transmission mechanism is demand’s impact on unemployment, underemployment, and insecurity in the labour market. The system is designed to enact this misery on a proportion of the population because conventional economic frameworks believe ‘there is no alternative’. Inherited from a NAIRU [1] framing where an unemployed buffer stock is treated as the anchor for price stability, today’s inflation control mechanisms are left seriously wanting.

Modern Monetary Theory (MMT) is a macroeconomic framework that switches the diagnostic lens through which to understand our monetary economy. It is an argument to stop treating artificial monetary scarcity as the governing constraint on fiscal policy and public provisioning, and to start treating the resource availability, market power, and distribution as what they are: the real battlegrounds of inflation (MMTUK, 2026).

This change in framing matters even more in a floating, non-convertible currency system. A currency-issuing state like the UK cannot be financially constrained in its own unit of account in the way a household or firm is. The binding constraints are inflation and productive capacity, ecological and planetary resource boundaries, plus the external constraint of what can be imported and on what terms.

It follows that once we understand that money is not a scarce commodity, but a monopoly of the state or its licensed agents (banks), the ‘stabilisation’ of the economy should be as flexible as possible to promote actual functional outcomes. Price stability and a balanced economy should be achieved by an institutional architecture that automatically expands and contracts nominal demand where slack exists, while also actively building, protecting, and reallocating real capacity when the constraint is on the supply side. Rigid fiscal rule frameworks are macroeconomically inefficient in this way, inappropriate for the dynamic needs of the economy, and consistently produce very poor human outcomes via austerity bias. Balanced government budgets are rarely commensurate with a balanced and efficient economy.

Inflation can be caused by demand or supply side factors. In the UK, major inflation episodes have often been driven primarily by supply shocks, including energy, food, imported inputs, and sectoral bottlenecks, though these can later feed into secondary cost-push pressures through wider wage and price dynamics. A responsible approach to managing these pressures must therefore employ the right tools for the right problem in an adaptable way.

The stabilisation toolkit set out here is thus an attempt to make a new architecture explicit and to provide, at the very least, a plausible alternative to the existing approach to tackling inflation. Simultaneously, these policies promote improved human wellbeing, more sustainable and long term policymaking, and a way of thinking about political economy that rejects the ideological rigidness of the neoliberal era.

It has seven mutually reinforcing components that combined produce a holistic inflation management framework:

A Job Guarantee (JG) as the core nominal and labour-market anchor and powerful automatic fiscal stabiliser.

Permanent Zero Interest Rate Policy (ZIRP) to end interest-rate fine tuning and its regressive side effects.

Bank Asset Regulation and Credit (BARC) policies to stop private credit from weaponising low rates into asset bubbles and to direct credit flows to socially productive development.

Universal Basic Services (UBS) and Social Housing to de-financialise essentials.

Active Fiscal Intervention to relieve bottlenecks and manage critical prices.

Import Space Management to deal with exchange-rate and import-cost pressures without punishing the poorest.

Strategic domestic capacity investment to reduce exposure to repeated supply shocks.

[1] Non-Accelerating Inflation Rate of Unemployment

Job Guarantee

The Job Guarantee is the headline part of fiscal dominance stabilisation because it shifts the adjustment mechanism from the money markets via interest rates to the labour market via the amount spent at a fixed nominal wage. The JG solves the conventional Phillips curve trade-off between unemployment and inflation and renders the notion of some ‘natural’ rate of unemployment an inapplicable concept, something long believed to be an unavoidable aspect of monetary economies by conventional macro literature (Clark, 1997). Instead of relying on a buffer of unemployed people to discipline wages, the state becomes the employer of last resort, offering a standing job at a fixed wage and conditions to anyone willing and able to work (MMT UK, 2026).

In this sense, the JG disciplines wage dynamics without disciplining workers. It replaces the blunt, asymmetric coercion of unemployment with a symmetric system in which both sides of the labour market face credible outside options. Workers can always exit to the JG without life-ruining loss of income or dignity, and firms can always recruit from a pool of people who are employed, socially integrated, and with relatively less skill fade without any pressure to bid up wages. The result is stabilised wage setting within a framework of full employment.

Mechanically, it is a powerful spend-side automatic counter-cyclical stabiliser. In a downturn, private demand falls, layoffs rise, and participation in the JG automatically expands. In an upswing, private employers hire from the pool by offering better wages and conditions, and the JG automatically contracts, cutting demand out of the economy to counteract the boom. This acts precisely like a buffer reserve providing additional supply on tap to prevent prices rising. The result is continuous full employment in the literal sense with anyone who wants paid work at the programme wage having it, without needing to ‘pump-prime’ aggregate demand to the point of overheating. This was a fatal flaw in Keynesian full employment policies which relied on generalised demand stimulus without having a nominal anchor or mechanism to discipline wages (Mitchell, 2011).

With a JG in place, the government’s net spending level (deficit/surplus) is set at the margin by the amount spent on JG wages. It fluctuates dynamically to inject the required demand to absorb labour slack in the places and times it’s needed, but importantly no more and no less.

The JG is designed to “hire off the bottom” where there is zero market bid, so it does not compete with private bids for already-employed labour in the way a generalised stimulus can. The initial act is a conversion of unemployment into employment at a fixed wage, which is precisely why it can serve as an inflation anchor rather than an inflation accelerant.

If the initial JG wage is set too high relative to the existing wage structure and prevailing productivity, it can cause a one-off price level adjustment as low-wage sectors reprice, but this is not inflationary in the dynamic, continuous sense. Once established, the JG wage anchors the rest of the labour market wage structure, along with prices set by firms as a markup over their costs (labour being a significant one).

A more tangible social argument for a JG is its pre-distributive impact. The real opportunity and social costs of demand-deficient unemployment are enormous and too often underestimated by conventional policy makers, and they compound. A standing offer of paid work strengthens labour market liquidity, preserves skills, and supports the long-run supply side by preventing scarring and by sustaining participation. In a currency-issuing state, persistent unemployment need not be a routine mode, but it is evidence of institutional failure to mobilise idle real resources while unmet social needs remain.

Permanent ZIRP

Once the labour market is anchored through a JG, the interest rate can be demoted from its current role as the primary stabilisation lever for price stability. That is where permanent ZIRP fits in.

Interest paid by the government on its stock of public debt is explicitly an exogenous policy variable. This insight, in contradiction to much of conventional economic thinking, derives from the observation that the state is a monopolist over its issue of tax credits (currency) and therefore is always able to set the price on its own liabilities once private sellers have accepted them in payment.

There is no market mechanism that is able to force such a state to pay a positive risk-free rate because there is no inherent requirement to drain net currency creation with government bond issuance and so there is no requirement to pay interest to induce sufficient demand for those bonds. To pay interest is therefore a choice regarding how much fixed rate duration policymakers wish to add to private sector currency savings.

Put simply, so-called ‘monetary financing’ is not inherently more inflationary than bond-financed net spending. Swapping between reserves, cash, and government bonds changes the form in which the private sector holds state liabilities, but it does not by itself create additional spending power because it is primarily a savings portfolio adjustment. That means the government can choose the yield curve it wants, allow private portfolios to settle across it, and leave any excess in zero-yield overnight reserves. That is a perfectly workable and sustainable model of debt management.

ZIRP matters because high policy rates carry three stabilisation costs that are treated as normal in the current regime.

Firstly, they distribute income upward by paying a risk-free return on state liabilities to whoever holds them, in proportion to their wealth. As the state is a net payer of interest, this is an explicit fiscal transfer channel and represents a regressive basic income policy.

Because wealth is extremely unevenly distributed, this fiscal choice disproportionately benefits those with substantial financial wealth in the form of interest-bearing savings (ONS, 2025). Distribution shapes behaviour, resilience, and the political sustainability of any counter-inflation policy and so any policy choice to inject spending onto private sector balance sheets in such a regressive way should be far more transparent and motivated, if, indeed, it is done at all.

Secondly, rate hikes can become conceptually ambiguous as an anti-inflation tool in high public debt, high-wealth economies. If government interest payments rise with rates, higher rates directly raise private interest income, and some of that is spent. Under some debt ratios and behavioural assumptions, that ‘interest income channel’ can offset the intended demand compression from the credit contraction and saving channels either significantly or altogether (Wray, 2013). ZIRP shuts that channel down at source and removes the potential ambiguity over the indirect effect on real economy demand that monetary policy can often produce.

Thirdly, using interest rates to try and manage inflation that is driven by supply shocks often amounts to treating a real resource constraint as if it were excess demand. The result is recessionary pressure without directly fixing the bottleneck. Recent inflation episodes in the UK have been heavily shaped by energy and food shocks and by supply disruptions, even if induced labour-market tightness later introduces additional cost-push inflationary pressures as supply impacts spread in the wider domestic economy (Haskel, 2023).

A regime that defaults to rate hikes as the first response is structurally biased toward unemployment as the adjustment variable and depending on interest elasticity of investment, higher rates can dampen the very supply-side expansion required to alleviate the inflationary pressure they’re trying to mitigate against in the first place.

Without complementary policies, low rates can induce excessive speculative and risk-taking activity in the financial and banking sectors as wealth holders rebalance portfolios to chase desired risk-adjusted returns. That is well documented, including by the Bank for International Settlements (BIS) and asset price inflation as well as destabilised financial conditions can often result (Gambacorta, 2009). So ZIRP only belongs inside a toolkit that also includes aggressive credit and bank asset regulation that can curtail such consequences. Which brings us to BARC.

Bank Asset Regulation and Credit Policies

No counter-inflationary stabilisation policy suite is complete without attention paid to the role private credit has in driving investment, production, economic cycles, and, too often, inflationary or destabilising financial bubbles. Commercial banks create broad money endogenously when they lend to creditworthy customers given prevailing regulation and competition constraints (Mcleay, Radia, & Thomas, 2014). The institutional design of our monetary and banking systems is such that required settlement balances (currency reserves) are then supplied reflexively to accommodate these credit flows to maintain a smoothly operating payments system and to ensure central bank monetary policy targets are met.

This means that many demand-pull inflationary dynamics are not primarily driven by government spending. They are driven by the scale and direction of private bank credit and the spending flows they enable. BARC is the suite of policies that recognises credit creation as a public privilege and therefore as a public policy domain in need of tight regulation to shape production and resource mobilisation to serve the long-term public interest.

The goal is to regulate the asset side of bank balance sheets so that credit creation preferentially supports productive and socially constructive activity and the capital development of the economy, while constraining credit that is primarily speculative, extractive, or destabilising.

There are two parts to this goal. One is straightforward macroprudential policy. Tools like loan-to-value and loan-to-income limits, sectoral capital requirements, and other tools available to financial regulators exist precisely because housing credit, asset booms, and leverage cycles can create systemic risk and spill into the real economy. This can be strengthened and serve to complement the wider toolkit here. The UK’s own institutional architecture for this, through the Financial Policy Committee (FPC) at the Bank of England, is explicit about the range of powers available to them to properly regulate the financial sector (Bennett, 2024).

Unfortunately, the UK’s recent experience shows how weak or poorly targeted regulation can create systemic fragility rather than productive investment. The 2022 turmoil in the UK gilt market exposed the extent to which pension funds had adopted highly leveraged Liability Driven Investment (LDI) strategies in order to chase marginal yield while managing long-term liabilities. When interest rates rose sharply, those strategies forced rapid gilt sales to meet collateral calls, amplifying market stress and requiring emergency intervention by the Bank of England to stabilise the system (Parliament, 2023).

Episodes like this illustrate that the financial sector’s incentives often do not naturally align with macroeconomic stability or productive capital formation. They also demonstrate the clear scope for stronger asset-side regulation to reduce speculative leverage and direct financial activity toward socially productive investment. We should divorce from the idea that allowing increasingly complex financial engineering to squeeze ever greater profits out of the system is somehow in the public interest or necessary for a stable and balanced economy to thrive.

The other part is credit guidance in the deeper sense. If the state can regulate bank lending standards to protect financial stability, it can also use regulation, public banking, and public guarantees to tilt credit toward the investments that expand real capacity, reduce supply constraints, and improve resilience over the long run. The incentives and outcomes of casino-like speculation are not aligned with long term capital formation and public purpose provisioning. This component of the toolkit looks to reject the more laissez-faire philosophical approach to banking that has dominated the financialised era of the last 40 years, even after the global financial crisis.

In this toolkit, BARC is the necessary counterpart to ZIRP. Zero risk-free benchmark rates provide significant benefit, but they must be paired with stronger controls on speculative credit creation and de-financialised housing and essentials provision so that the system’s response is investment and capacity rather than another leveraged asset cycle which in itself can be highly regressive.

Universal Basic Services and Social Housing

A large share of what households experience as inflation is concentrated in essentials. Housing, domestic energy, food, transport, childcare, health access, and care are either structurally non-substitutable or politically non-negotiable. When these are provisioned primarily through increasingly financialised private markets, they become persistent sources of cost pressure and precarity.

Universal Basic Services (UBS) responds by shifting part of the basic consumption bundle from market provisioning to collective provisioning as a right of access to meet basic needs rather than as a function of ability to pay. The clearest UK articulation of UBS comes from work associated with UCL’s Institute for Global Prosperity and the New Economics Foundation (NEF), defining UBS as collectively generated activities that serve the public interest, available to all at a level sufficient to meet basic needs (Coote, Kasliwal, & Percy, 2019).

The stabilisation relevance is not that UBS somehow abolishes scarcity. It is that it changes the inflation and distributional dynamics across the economy. If core essentials are guaranteed directly, households are less forced into debt-driven coping strategies, and wage demands are less pressured by private consumption price pass-through, particularly rent, energy and food price rises.

Social housing is the best example of how this becomes directly anti-inflationary. Social housing is defined by the OECD as residential rental dwellings provided at below-market prices and allocated through specified rules (OECD, n.d.). In England, the share of housing for affordable or social rent has fallen over recent decades, which increases exposure to private rent volatility and deepens housing-benefit pressures (Cromarty, 2024). Precarity and instability reign when housing becomes excessively financialised and serves too often as a speculative investment good.

A serious social housing programme is not only a distributional and social policy, pre-distributing wealth and power, but a direct attack on a major channel through which cost-of-living shocks translate into macro instability and inflationary bias. It reduces the economy’s sensitivity to the precise categories where private market cost-push inflation is most socially and politically explosive.

Active Fiscal Intervention

One of the most corrosive myths in economic discourse is that fiscal policy is neutral in the long run. That perspective only looks plausible if you assume a frictionless supply side and path independence. Neither assumption survives contact with how large parts of the real economy actually price output or respond behaviourally to changes in fiscal policy.

There is an extensive literature supporting the observation that firms price output on a cost-plus-competitive-mark-up basis (Hall, Walsh, & Yates, 1997). Supply shocks hit unit costs, and price increases are the normal response, expressed through mark-ups and shaped by market structure. The OECD’s work on competition and inflation also highlights how market power shapes cost pass-through dynamics (OECD, 2022).

So, if the inflation is coming from bottlenecks, input-price spikes, or concentrated market power, an “active fiscal state” has to operate at the level of the bottleneck or anti-competitive sector, not at the level of generalised demand suppression. Bottlenecks in supply chains propagate cost-push inflationary pressures throughout the rest of the economy, potentially far before generalised full employment capacity is realised. This cost shock can then couple into labour market pressures as both labour and capital fight it out over who maintains their real share of national income. It can therefore be significantly counter-inflationary for the state to actively intervene via fiscal policy as early as possible in this cycle where the state can genuinely ease the bottleneck.

The primary lever to enact such intervention is investment in targeted capacity expansion and reallocation. Supply bottlenecks were a major driver of inflation pressures in the post-pandemic period, and even the International Monetary Fund (IMF) has published analysis showing how bottlenecks hurt output and boosted producer prices and overall inflation in 2021 (Celasun, 2022). If the problem is port capacity, logistics, grid constraints, childcare supply, retrofit labour, or planning bottlenecks, then the anti-inflation action is to fix those constraints, even if that requires upfront spending. Done correctly, that raises the real supply ceiling and reduces medium-term inflation risk. Generalised demand suppression via rate hikes is rarely a suitable or effective medicine.

The second important lever is critical-price management. It is useful to recognise that some prices are systemically important, and that temporary price stabilisation can be preferable to allowing market sectoral price shocks to feed into wider inflationary dynamics. The policy details matter, and broad ‘price controls’ can be poorly designed and sometimes counterproductive, but there is now a serious policy literature on targeted interventions in major price shocks, especially in energy where forms of price controls on producers can have significant disinflationary effects (Rulz, Schult, & Wunder, 2024).

The third lever is discretionary fiscal stance discipline where demand can really be the problem. Government procurement frameworks and fiscal budgeting via functional finance principles must be laser focused on real resource availability and potential inflationary pressures. For instance, spending bills for projects should not be authorised in Parliament before analysis is conducted on their inflationary potential. Adopting a price rule principle where procurement is conducted at current prices where quantity and pace is allowed to adjust (when possible) to prevent government fiscal bids pushing the general price level up, also supports stabilisation.

The JG handles a large part of the automatic demand stabilisation job. Therefore, discretionary fiscal tightening should be used only when and where spending is genuinely outrunning capacity. And it should certainly not be the default response to supply shocks.

Import Space Management

The most common fear story about an active fiscal state is a story about market punishment, capital flight, and currency collapse leading to imported inflation. This fear is often narrated as if we were still in a fixed-rate convertible currency world, where worsening external balances mechanically force domestic austerity. But in a modern floating-rate system, the dynamics are different and policy space is expanded.

A flexible exchange rate regime maximises domestic policy space precisely because it removes the obligation to defend a peg and to subordinate domestic employment to external balance targets (Mitchell, 2018). Capital flight in the simplistic sense does not literally drain sterling out of the system because for every seller of sterling assets there is a buyer and what adjusts is the price, meaning the exchange rate. Sterling balances remain as liabilities recorded on the Bank of England’s balance sheet.

If a shift to permanent ZIRP reduced the interest rate differential that currently attracts some financial flows into sterling, it is possible that the currency would initially trade at a lower level. But a lower price does not eliminate demand for sterling. Any buyer in this context is not seeking to save in a high yield currency but likely seeking to spend it, either by buying UK exports, or by investing in UK capital formation or asset markets. This can be stimulative and reflect broader capital flows.

More importantly, policy changes do not occur in isolation. A macroeconomic regime that maintains genuine full employment, stable demand, and sustained public and private investment in productive capacity and improved human capital can itself strengthen the underlying attractiveness of the domestic economy. These material longer term improvements are likely to crowd in foreign demand for sterling and support the UK’s real import space. The result need not be a permanently weak currency or runaway imported inflation as many conventional narratives fear. It may simply be a different equilibrium in which sterling reflects the productive strength of the UK economy rather than being supported by high interest rates paid to global savers.

The implication is that the UK does not need to rely indefinitely on high interest rates as a form of subsidy to attract foreign capital. Exchange rates in floating systems are shaped by a much wider set of forces than rate differentials alone, and a strategy centred on full employment, investment, and productive capacity can be just as important in sustaining long-run demand for a currency and capacity to obtain what we need from the rest of the world.

A currency depreciation, should it occur, can indeed raise the domestic price of imports though, even if pass-through is laggy and weak, and the UK is structurally import-dependent in important categories. This means that stabilisation policies to manage shifting real terms of trade in the short term cannot ignore these exchange rate shifts, but they can be conducted without domestic austerity and unemployment.

Two empirical realities help here. The first is that exchange rates are heavily influenced by financial and capital flows and portfolio preferences, not just by trade flows which are a minor component of determining FX movements. Global FX turnover is enormous, in the multiple-trillions-per-day range, which is clear evidence that cross-border asset trades and hedging dominate the gross flows. The second is that international institutions themselves treat exchange-rate flexibility as a shock absorber, while also acknowledging that it does not always offer full insulation and that capital flow management can be part of the toolkit in some circumstances (Gelos & Sahay, 2023).

“Import space management” is the translation of these facts into a distributional stabilisation policy. If the problem is a terms-of-trade hit or a capital-flow-driven depreciation that raises import prices, the state can protect essentials and compress non-essential import demand instead of letting the shock hit the poorest hardest. In practice, that means using taxes, bans, controls, standards, quotas, and procurement policies to reduce luxury or high-import-intensity consumption in an emergency, freeing import capacity for food, energy, and critical inputs. It also means targeted subsidies or direct provision for essentials rather than untargeted cash that bids up constrained imports (Amaglobeli, 2023).

Full employment, stable zero base rates, elevated but stable demand levels, and increased public and domestic private investment can, under many conditions, support currency demand by improving the attractiveness of domestic production and domestic assets. It is not guaranteed, and it is not the only driver, but it is a serious counterweight to the panic story that assumes expansionary fiscal policy within available capacity automatically triggers currency collapse and unavoidable imported inflation (Wray, 2014). The correct question is: what does the policy change do to real capacity, human capital, institutional stability, and expected future production?

Strategic Domestic Capacity

The 21st century is increasingly demonstrating that old confidence in the long run benefits of global free trade and lowest-cost approaches to industrial development lack strategic insight and contribute to hollowing out of domestic productive capacity right when it is most needed to confront the polycrises of climate, ecological, and geopolitical constraints.

The case against this purist globalisation story is now mainstream. Repeated shocks have shown that brittle supply chains amplify inflation and output loss, particularly in essentials such as agricultural and energy products. The OECD has published explicit policy work on building supply chain resilience and on preparedness, including tools and frameworks for governments to identify and manage critical vulnerabilities (OECD, 2025). And economists such as Mariana Mazzucato have emphasised the importance of a collective response to global challenges, with an active fiscal state shaping long run outcomes for sustainable development and resilient public purpose provisioning (Mazzucato, 2023).

Strategic domestic capacity does not mean isolated and excessively protectionist autarky. It means deliberately maintaining, building, or regenerating capabilities in sectors where import dependence is an inflation and security risk. Food, energy, critical materials, industrial components, and key public-service supply chains are essential areas of production that should be invested in domestically to the maximum practical degree.

Real beneficial trade flows will continue though as we will never be able to produce everything we need at home. Our capacity to import is a function of what we can produce for export and how much sterling the foreign sector wants to save and so key natural and mineral resource imports are still readily obtainable as long as we invest in maintaining sustainable and attractive export markets, likely in science and technology, high-end engineering, and range of valuable knowledge services. But it is disinflationary over the long term to have strategic autonomy in key sectors and consumables.

A system that is structurally exposed to fossil fuel price shocks imports inflation through the energy channel. The International Energy Agency (IEA) is clear that a transition toward a more electrified, efficient, renewables-rich system reduces exposure to fossil fuel price volatility, even if risks remain (IEA, 2024). UK institutions increasingly make the same security argument. The Climate Change Committee (CCC) explicitly frames net zero as protection against fossil fuel price shocks, alongside broader benefits (CCC, 2026). Domestic investment in building up clean energy infrastructure and energy efficiency capacity is therefore a key counter-inflationary policy in the long term.

Strategic domestic capacity investment is the deliberate enlargement of the real resource envelope within which fiscal policy can operate without inflation and within which planetary and ecological boundaries are respected. It is also how you reduce the frequency and severity of import-space crises. If you can produce more of what you need domestically, the exchange rate and external supply shock risks matter far less for baseline living standards, and the distributional stakes are lower.

Conclusion

The core argument of this essay is that monetary dominance for inflation control and macroeconomic stabilisation is not good policy. In fact, I contend that continuing to adopt this conventional approach is a failing strategy for both people and planet.

The current stabilisation regime relies overwhelmingly on interest rate adjustments and labour market insecurity to restrain inflation. It is a blunt and socially costly approach that attempts to compress demand even when the underlying pressures originate from supply shocks, financial speculation, or structural bottlenecks. The result is a system that tolerates persistent unemployment, underinvestment in real capacity, and repeated vulnerability to the same inflationary shocks.

An MMT-informed framework points towards a different architecture. The Job Guarantee establishes a labour market anchor that secures price-stable full employment while stabilising wage dynamics and permanent ZIRP removes a regressive and often ambiguous monetary policy lever. Bank asset regulation and credit guidance ensure that private credit creation supports productive development rather than speculative cycles and universal basic services and social housing reduce the financialisation of essentials and dampen the most politically and socially destabilising forms of inflation.

Alongside these structural pillars, an active fiscal state can intervene directly to relieve supply bottlenecks, stabilise critical prices, and expand productive capacity where it matters most. Import space management protects living standards when external shocks occur, and strategic domestic investment reduces exposure to those shocks in the first place by strengthening the real sovereign resource base of the economy over the medium to long term.

Taken together, this toolkit replaces a stabilisation regime built on scarcity and insecurity with one built on resilience, capacity, and functional outcomes. Inflation tolerance and ecological and planetary boundaries remain the binding constraints for a currency-issuing state, but the way we operate our economies within these boundaries can be far better.

In a world of multiple overlapping crises and shocks, building such a stabilisation regime is increasingly necessary for both political and economic continuity and social wellbeing.

References

Amaglobeli, D. (2023). Policy Responses to High Energy and Food Prices. IMF.

Bennett, W. (2024). The contribution of the Financial Policy Committee to UK financial stability. London: Bank of England. Retrieved from https://www.bankofengland.co.uk/quarterly-bulletin/2024/2024/the-contribution-of-the-fpc-to-uk-financial-stability

CCC. (2026, March 11). Cost of Net Zero by 2050 less than a single fossil fuel price shock. Retrieved from https://www.theccc.org.uk/2026/03/11/cost-of-net-zero-by-2050-less-than-a-single-fossil-fuel-price-shock-ccc

Celasun, O. (2022). Supply Bottlenecks: Where, Why, How Much, and Where Next? Retrieved from International Monetary Fund: https://www.imf.org/-/media/files/publications/wp/2022/english/wpiea2022031-print-pdf.pdf

Clark, P. (1997). Phillips Curves, Phillips Lines and the Unemployment Costs of Overheating. International Monetary Fund. Retrieved from https://www.imf.org/external/pubs/ft/wp/wp9717.pdf

Coote, A., Kasliwal, P., & Percy, A. (2019). Universal Basic Services:: Theory and Practice. London: Institute of Global Prosperity, UCL. Retrieved from https://discovery.ucl.ac.uk/id/eprint/10080177/1/ubs_report_online.pdf

Cromarty, H. (2024). Affordable housing in England. London: House of Commons Library. Retrieved from https://commonslibrary.parliament.uk/affordable-housing-in-england/

Gambacorta, L. (2009). Monetary policy and the risk-taking channel. BIS Quarterly Review. Retrieved from https://www.bis.org/publ/qtrpdf/r_qt0912f.pdf

Gelos, G., & Sahay, R. (2023). Shocks and Capital Flows: Policy Responses in a Volatile World. International Monetary Fund.

Hall, S., Walsh, M., & Yates, A. (1997). How do UK companies set prices? London: Bank of England.

Haskel, J. (2023). UK inflation since the pandemic: how did we get here and where are we going? London: Bank of England. Retrieved from https://www.bankofengland.co.uk/-/media/boe/files/speech/2023/november/uk-inflation-since-the-pandemic-how-did-we-get-here-and-where-are-we-going-speech-by-jonathan-haskel.pdf

IEA. (2024). Strategies for Affordable and Fair Clean Energy Transitions. International Energy Agency.

Lerner, A. (1946). Functional Finance and the Federal Debt. Retrieved from https://public.econ.duke.edu/~kdh9/Courses/Graduate%20Macro%20History/Readings-1/Lerner%20Functional%20Finance.pdf?

Mazzucato, M. (2023). A collective response to our global challenges: a common good and ‘market-shaping’ approach. London: UCL Institute for Innovation and Public Purpose.

Mcleay, M., Radia, A., & Thomas, R. (2014). Money creation in the modern economy. London: Bank of England. Retrieved from https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2014/money-creation-in-the-modern-economy.pdf

Mitchell, B. (2011). Austerity proponents should adopt a Job Guarantee. William Mitchell Modern Monetary Theory. Retrieved from https://billmitchell.org/blog/?p=14208

Mitchell, B. (2018, September 26). MMT and the external sector - redux. Retrieved from https://billmitchell.org/blog/?p=40433

MMT UK. (2026). A COUNTER-INFLATIONARY JOB GUARANTEE FOR THE UNITED KINGDOM. MMT UK. Retrieved from https://mmtuk.org/research/job-guarantee/

MMTUK. (2026). Education. Retrieved from MMTUK Policy Research Group: https://mmtuk.org/education/

OECD. (2022). Competition and Inflation. OECD.

OECD. (2025). Keys to resilient supply chains. OECD.

OECD. (n.d.). Affordable Housing. Retrieved 2026, from OECD: https://www.oecd.org/en/topics/sub-issues/affordable-housing.html

ONS. (2025). Household total wealth in Great Britain: April 2020 to March 2022. Office for National Statistics. London: Office for National Statistics. Retrieved from https://www.ons.gov.uk/peoplepopulationandcommunity/personalandhouseholdfinances/incomeandwealth/bulletins/totalwealthingreatbritain/april2020tomarch2022?

Parliament, U. (2023). Leveraged LDI strategies worsened September 2022 financial turmoil. London: UK Parliament. Retrieved from https://committees.parliament.uk/committee/517/industry-and-regulators-committee/news/185963/leveraged-ldi-strategies-worsened-september-2022-financial-turmoil/

Rulz, M. H., Schult, C., & Wunder, C. (2024, November 18). The effects of the Iberian exception mechanism on wholesale electricity prices and consumer inflation: a synthetic-controls approach. Applied Economic Letters, 1(7).

Wray, L. R. (2013). Did Scott Sumner Find MMT’s Achilles Heel? Retrieved from https://neweconomicperspectives.org/2013/11/scott-sumner-find-mmts-achilles-heel.html?

Wray, L. R. (2014). MMT and External Constraints.

I appreciate the argument here, especially the critique of using unemployment as the blunt instrument of inflation control. But I wonder whether this essay underplays the corruption risk built into monetary elasticity itself…

Any system that permits discretionary creation of purchasing power creates a first-receiver problem (aka Cantillon effects). Whether through QE, deficit spending, bank credit, or emergency liquidity facilities, new money does not enter the economy evenly. It enters through institutions closest to the monetary spigot (ie The FED and banks), then works its way outward as higher asset prices, higher living costs, and deeper dependence on public debt.

So the question may not only be whether we can replace rate hikes with better fiscal tools. The harder question is whether any discretionary monetary regime can avoid becoming a political allocation machine a la “absolute power corrupts absolutely”. At some point, real resilience may require not just better management of money, but harder limits on who gets to create it in the first place.

Great read, thanks Jamie. A couple of thoughts:

- a very minor point: I think the wording “[money is] a monopoly of the state or its licensed agents (banks)”, you probably mean “the state and its licensed agents.” The monopoly is the state’s and its licensed agents simply act under the terms of their licenses; and

- a meatier point: a missing item in your seven-part inflation fighting toolkit is antitrust law. If we think of the recent post-Covid inflation episode - sellers inflation - that was driven by huge market power from highly concentrated markets, where CEOs literally bragged to their shareholders about hiking prices under the fig leaf of Covid impact on trade. We only have to look at the work Lina Khan started in her short time at the FTC to understand the impact of muscular antitrust in terms of freeing up bottlenecks.

Love your work!